After all, the market has consistently risen and fallen on many occasions over the last 100 years or so: it’s what it does. Over time, markets recover. So, in the years leading up to retirement, as long as you don’t cash in any losing investments, the sequence of returns doesn’t matter too much.

However, this is not the case once you retire. At that point, you’ll switch from growing your wealth to drawing from it to provide yourself with retirement income. This is when the sequence of returns becomes really important and can have a huge impact on how long your savings will last.

What is sequence of returns risk?

Sequence of returns is the order in which your investment returns (gains or losses) happen. Sequence of returns risk is when the market declines when you first retire and/or start withdrawing income, leaving you with less money to grow, meaning your savings could run out too soon.

How the sequence of returns risk impacts retirees

When you first retire, it’s not wise to put all your money into a cash savings account. Canadians are living much longer than even a couple of generations ago, with the average Canadian life expectancy being just over 83. You may therefore need your money to last 20 years or even more, which means you’ll probably need returns that are considerably higher than the interest you’ll find in a typical savings account.

You also need to ensure that your money doesn’t lose its value, so you need returns that can keep up with (or exceed) the rate of inflation. To accomplish this, your portfolio needs to be comprised of both equities (shares in publicly traded companies) and fixed income (typically bonds, which are loans made to governments and companies). Equities provide greater growth potential, while fixed income assets typically provide more security.

When you start withdrawing money from your retirement savings, you open yourself up to sequence of returns risk. This is because regular withdrawals reduce the overall value of your portfolio, which is the basis for all future compound growth.

If your portfolio were to lose value (have negative returns) in the early stages of withdrawing income from it, the base amount that can generate positive returns would become so much smaller, meaning you’d have fewer investments to grow or compound once the market recovers.

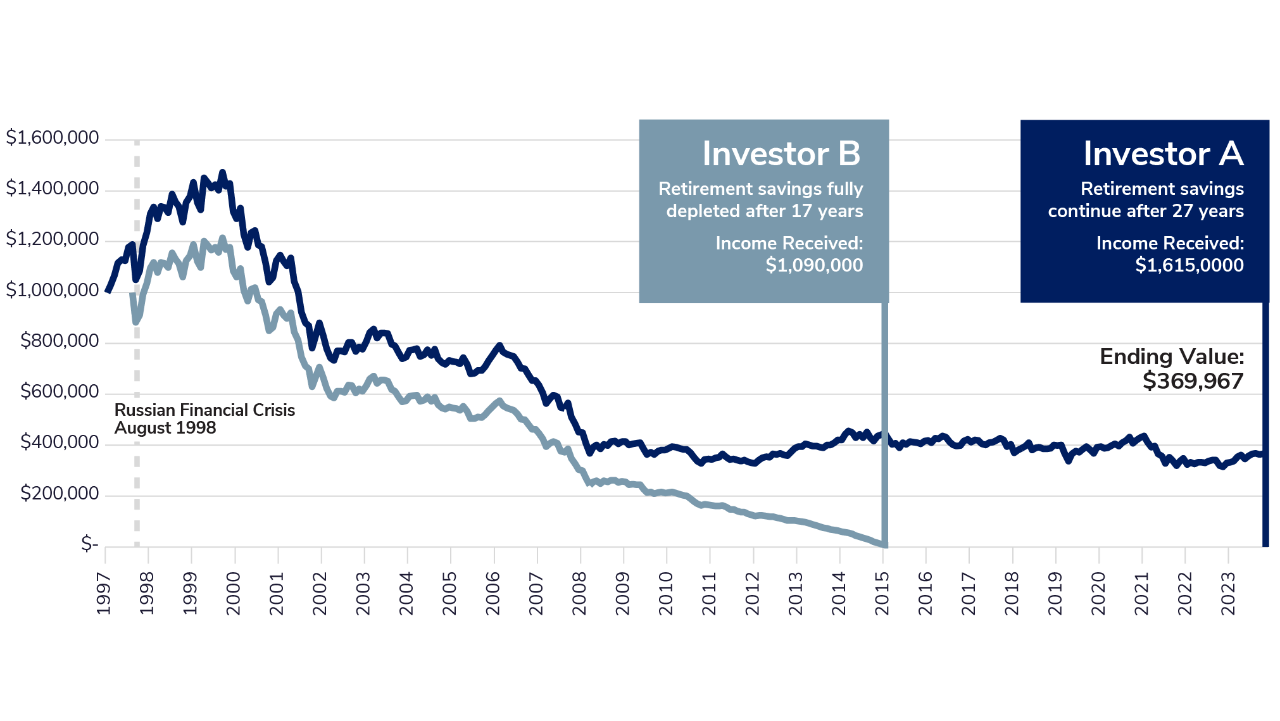

How sequence of returns risk can cause very different outcomes

Let’s look at an example of two investors, Investor A and Investor B, who both retired with $1 million in savings in 1998, the year of the Russian financial crisis. This crisis was caused by Russia defaulting on its debts, which led to financial problems for countries that exported to it. The Russian rouble was heavily devalued, and global equity markets were hit hard (albeit for only a short period of time).

Investor A

They started their retirement on January 1 of that year, and by the time the crisis began, had experienced several months of positive returns and seen their $1 million in investments grow to almost $1,189,000. A month after the crisis, these investments had dropped to just over $1,055,000. However the markets recovered and Investor A’s savings ended the year at over $1.3 million.

Investor B

They didn’t retire until July, just before the Russian financial crisis began. Their $1 million in investments quickly dropped in value to almost $883,000 in just a month. By the end of the year, their investments had also recovered and finished the year at almost $1.1 million.

The damage had been done, however, with Investor B having over $200,000 less in savings than Investor A. As we can see in the chart below, Investor B’s money had completely run out by 2015. Investor A, on the other hand, still had over $400,000 in savings at that point. By 2024, their savings were still at almost $370,000.

How to manage sequence of returns risk

There are several ways to mitigate sequence of returns risk. Given that withdrawing income from a portfolio that has lost value is the key to sequence of returns risk, one way to minimize risk is to have other sources of income readily available if the market drops.

Maintaining exposure to equities in your retirement portfolio is crucial. Equities offer growth potential that can help mitigate risks like longevity and inflation. However, it's wise to choose investments that not only provide equity exposure but also offer proven protection when markets decline; this will ensure the stability of your income stream.

You could also buy a term annuity, which will provide you with a regular income for a set period of time (for example, the next five years) regardless of how the markets perform. This way, if there is a market crash at the beginning of your retirement, you can leave your investments untouched for five years. After that time, your investments should have recovered and increased in value, so you can start to draw income from them (or buy a new annuity to cover the next five years).

Finally, a cash reserve strategy involves putting some of your assets into cash (or cash equivalents) to cover periods of potential market decline. For example, you could hold three years’ worth of retirement income in cash equivalents, like guaranteed investment certificates (GICs). These are very safe investments, with guaranteed interest rates and different terms, such as one, three and five years.

If the market crashes, rather than withdrawing money from investments that have dropped in value, you could cash in your short-term GICs. If the stock market crash persists for several years, you could then cash in your mid- and long-term GICs when you need the money. This strategy ensures that you don’t touch any assets affected by the market crash, and so it helps you avoid sequence of returns risk.

Help with minimizing sequence of returns risk

Your IG Advisor will be able to suggest the best strategies to avoid sequence of returns risk, based on their knowledge of your overall financial plan. What works for one investor might not be appropriate for another, so it’s important to adopt the strategy that’s right for your individual circumstances.

If you’re approaching retirement, call your IG Advisor to discuss the best strategies to minimize sequence of returns risk for you. If you don’t have an IG Advisor, you can find one here.

1 For the purposes of these examples, we use simple returns, rather than compound returns.

Written and published by IG Wealth Management as a general source of information only. Not intended as a solicitation to buy or sell specific investments, or to provide tax, legal or investment advice. Seek advice on your specific circumstances from an IG Wealth Management Advisor.

GICs issued by Investors Group Trust Co Ltd., and/or other non-affiliated GIC issuers. Minimum deposit, rates and conditions are subject to change without notice. Commissions, fees and expenses may be associated with mutual fund investments. Read the prospectus before investing. Mutual funds are not guaranteed, values change frequently and past performance may not be repeated. Mutual funds and investment products and services are offered through Investors Group Financial Services Inc. (in Québec, a Financial Services firm). And Additional investment products and brokerage services are offered through Investors Group Securities Inc. (in Québec, a firm in Financial Planning). Investors Group Securities Inc. is a member of the Canadian Investor Protection Fund. Written and published by IG Wealth Management as a general source of information only. Not intended as a solicitation to buy or sell specific investments, or to provide tax, legal or investment advice. Seek advice on your specific circumstances from an IG Wealth Management Advisor.

Insurance products and services distributed through I.G. Insurance Services Inc. (in Québec, a Financial Services Firm). Insurance license sponsored by The Canada Life Assurance Company (outside of Québec).