Guardian Capital Global Dividend

Mandate commentary

Q1 2026

Mandate overview

The mandate performance this quarter was driven by a combination of positive sector allocation and stock selection effects. The energy sector was the fund’s largest contributor to relative performance, driven by its overweight exposure, which was slightly offset by negative stock selection from Williams Companies and Shell. Darden Restaurants, TJX and McDonald’s added to relative performance in the consumer discretionary sector. The health care sector contributed to relative performance on strong stock selection from AstraZeneca and Johnson & Johnson. Similarly, the real estate sector contributed, thanks to a robust performance from Equinix. On the flip side, the fund’s underweight exposure to the materials and utilities sectors was a drag on performance this quarter.

The mandate performance this quarter was driven by a combination of positive sector allocation and stock selection effects. The energy sector was the fund’s largest contributor to relative performance, driven by its overweight exposure, which was slightly offset by negative stock selection from Williams Companies and Shell. Darden Restaurants, TJX and McDonald’s added to relative performance in the consumer discretionary sector. The health care sector contributed to relative performance on strong stock selection from AstraZeneca and Johnson & Johnson. Similarly, the real estate sector contributed, thanks to a robust performance from Equinix. On the flip side, the fund’s underweight exposure to the materials and utilities sectors was a drag on performance this quarter.

Mandate: Guardian Capital Global Dividend portfolio stock review.

Performance contributors

ASML was the strategy's strongest relative performer. The company occupies a structurally unique position as the sole manufacturer of extreme ultraviolet lithography systems, a near monopoly in the most critical piece of capital equipment required to produce advanced semiconductors. ASML closed 2025 with a record backlog (nearly double analyst forecasts), driven by accelerating AI-related demand, and strong guidance for 2026 revenue. ASML’s infrastructure enables AI and is therefore not a business model threatened by it. ASML has a dominant competitive moat, highly visible contracted revenue, pricing power and a growing dividend.

Equinix contributed to relative performance, with the company issuing 2026 revenue guidance above consensus estimates, due to the surge in demand for specialized AI data centres. Critically, Equinix's business model generates highly recurring, contractually based revenues, insulating it from the software disruption narrative that weighed on application software stocks. Record fourth-quarter bookings reinforced the company's positioning. Equinix raised its quarterly dividend by 10%, marking its 11th consecutive year of dividend growth. During the quarter, investors rewarded the company’s quality profile, income growth and earnings visibility.

Performance detractors

Williams Companies detracted from relative performance, despite being up approximately 21% during the quarter. The relative performance drag is primarily due to the quarter's unusual dynamics rather than any fundamental deterioration in the business. Williams is a high quality midstream natural gas infrastructure company with predominantly fee-based, volume-driven contracts that largely insulate it from direct commodity price exposure. However, following the onset of the Iran conflict, the energy sector rallied sharply, but Williams underperformed the energy sector broadly, creating a relative performance drag in a quarter where energy was the top-performing sector.

Microsoft detracted from relative returns. As one of the world's largest software businesses, Microsoft was at the centre of the software disruption narrative that drove the early quarter sell-off. Enterprise software equities experienced significant valuation compression, as the rapid proliferation of agentic AI began to erode confidence in the per-seat licensing model that has underpinned software economics for two decades. Microsoft's exposure spans both the threatened software segment and the potentially beneficial infrastructure segment, through Azure cloud infrastructure and its own AI platform investments. The market, however, weighted the near-term disruption risk more heavily than the long-term AI infrastructure opportunity. Microsoft's elevated valuation and growth classification placed it squarely in the cohort most penalized during the first quarter’s rotation towards defensives.

Total gross returns:

Total return | QTD | YTD | 1YR | 3YR | 5YR | SINCE INC. (FEB. 18, 2025) |

GUARDIAN CAPITAL GLOBAL DIVIDEND | 1.29

| 1.29 | 14.75 | 8.65

|

Mandate repositioning

Last year, the portfolio activity remained light, as reflected in the low turnover. The trades executed so far this year fall into three key themes.

First, in a market defined by regime shifts, the focus was on recognizing structural breaks early. When the GEMX model flagged deteriorating trends in earnings or dividend growth, the team did not hold on to losers and moved decisively to reduce exposure.

Second, as noted earlier in the “AI Capex paradox” discussion, the team identified weakness in SaaS-linked business models as early as summer 2025. A high conviction exit from Accenture and trims in Wolters Kluwer added meaningful value, particularly when viewed from January 2026.

Third, the team stays on top of emerging leaderships through the lens of earnings growth AI. This has created a healthy pipeline of opportunities to rotate into as structural change advances.

During the quarter, the team initiated positions in Amphenol and Vistra. GEMX forecast strong earnings per share (EPS) growth going forward, with a low probability of earnings drops. For the information technology sector, Amphenol boasts top decile forecast dividend growth, with past dividend growth in the double-digit range with a very low probability of dividend cuts. Vistra is one of the largest competitive power generators in the U.S. The team continues to see massive tailwind from AI-driven power demand, as data centres reshape U.S. electricity markets; Vistra looks like becoming one of the biggest beneficiaries.

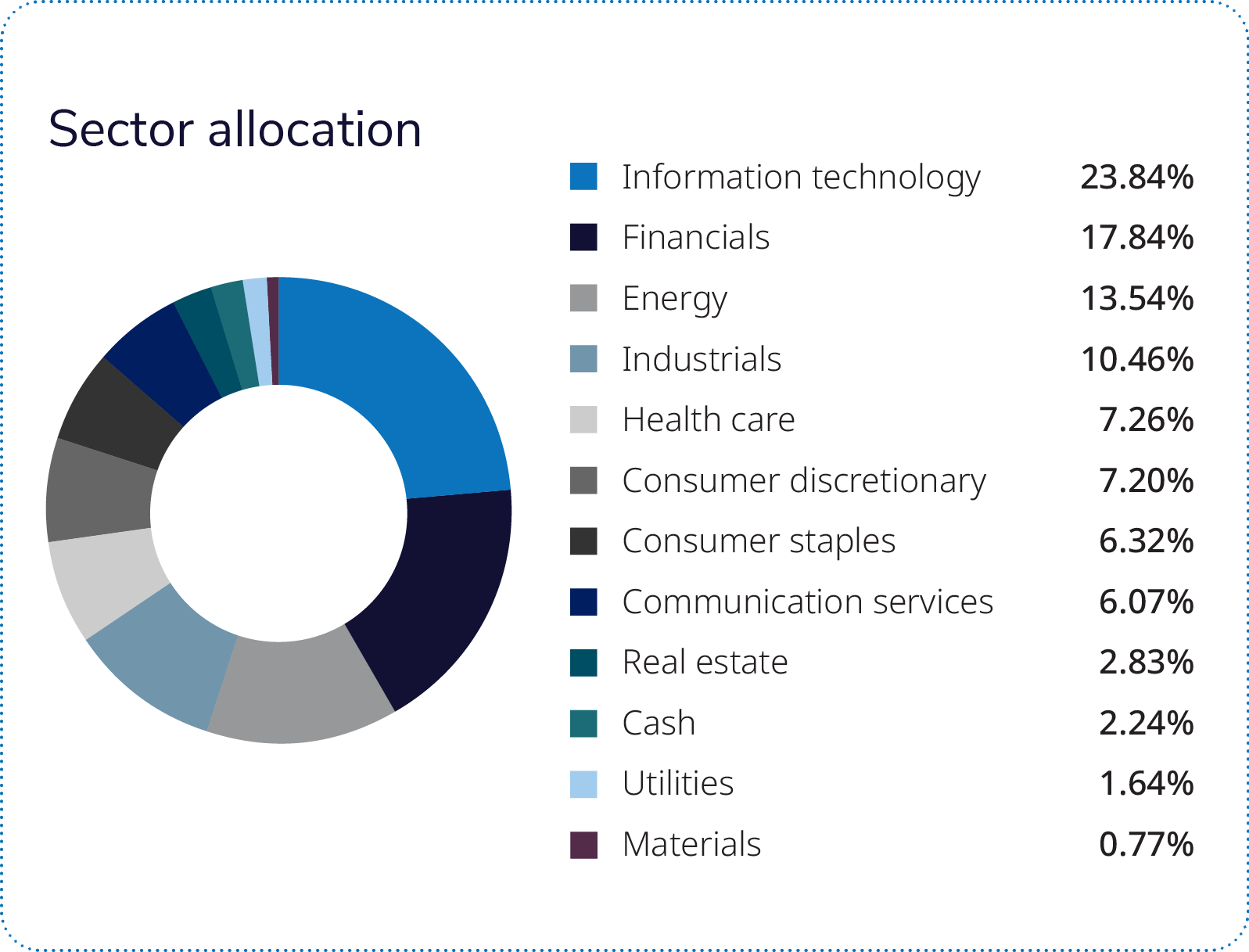

The mandate is overweight the energy, consumer staples and financials sectors, and underweight the materials, communication services, consumer discretionary and information technology sectors. Regionally, the strategy has approximately 26% weight in Europe, 73% weight in North America and 1% weight in Asia.

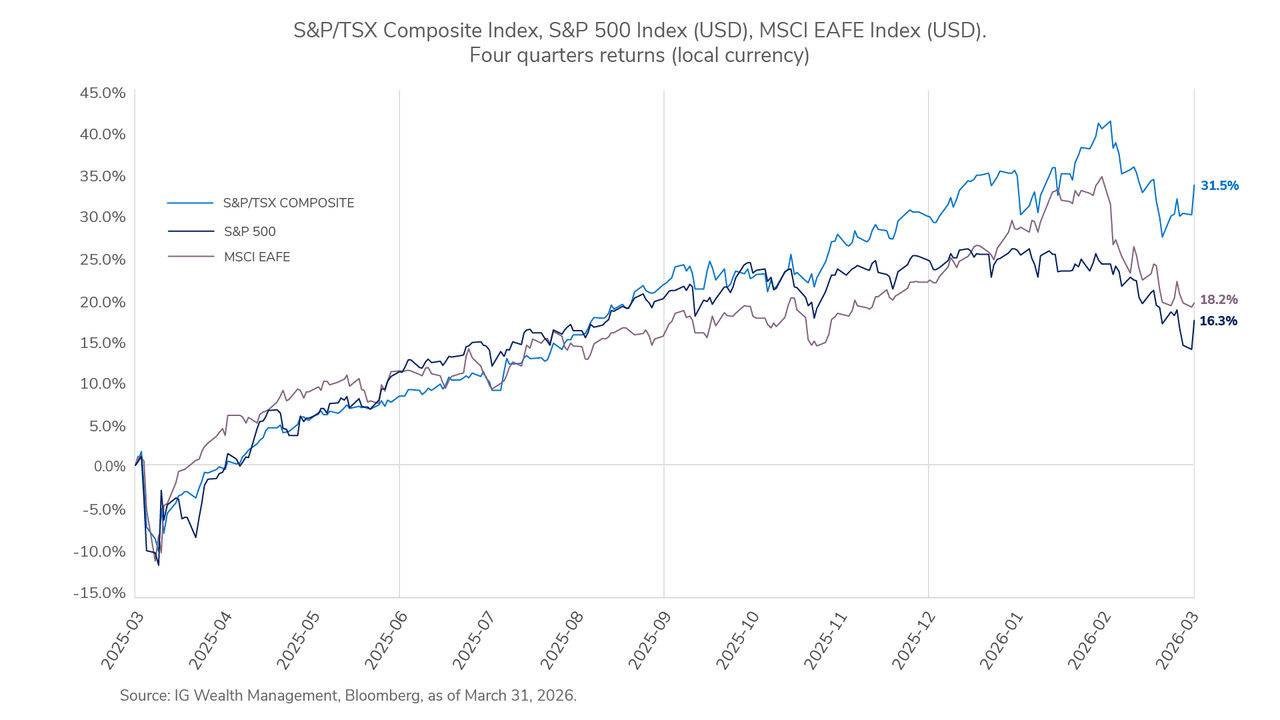

Market overview: oil shock drove turbulence, commodities dominated inflation fears

The first quarter of 2026 began with supportive economic momentum; improving manufacturing, a stabilizing U.S. housing backdrop and contained inflation. However, this quickly pivoted as the conflict in the Middle-East involving Iran — along with trade disruption around the Strait of Hormuz — pushed energy commodities higher. The energy shock drove volatility across global equities, yet the underlying backdrop proved more resilient than headlines implied, reinforcing the value of diversification.

Canadian equities were resilient, as higher crude oil prices supported the energy sector and helped offset weaknesses in rate-sensitive areas. Defensive sectors, dividends and real-asset exposure provided additional insulation versus many global peers. U.S. fundamentals remained solid, but sentiment weakened as oil lifted inflation expectations. Investors rotated away from expensive, rate-sensitive growth stocks, making performance more about a valuation reset than deteriorating earnings.

Market outlook: global growth expectations will be adjusted if conflict extends beyond summer

Looking ahead, oil and energy prices remain the central swing factor. A credible path to de-escalation could shift attention back to the positive economic cycle evident early in the quarter; a prolonged disruption would maintain inflation uncertainty and elevated volatility.

In this environment, commodity producers and value‑oriented equities may provide resilience, while long‑duration assets and oil‑importing regions face greater sensitivity to energy-price fluctuations.

Diversification and flexibility remain central to portfolio construction

Canadian equities offer exposure to energy and materials supported by global supply constraints. International developed and emerging markets present valuation‑driven opportunities and help diversify away from concentrated U.S. equity exposure.

Within fixed income, short‑ to intermediate-duration strategies can balance yield and interest‑rate risk, complemented by high‑quality corporate bonds for disciplined income generation. Key areas to watch will be central bank policies, as they look at the impact of higher energy costs and their indirect tax on the consumer.

To discuss your investment strategy, speak to your IG Advisor.

Azure Managed Investments™ provides discretionary investment management services distributed by IG Wealth Management Inc., Investment dealer. We will manage your Azure Managed Investments Accounts on a segregated basis in accordance with your investment policy statement and the resulting mandate selected by you. Mandates will be managed by I.G. Investment Management, Ltd. and partner organizations. You are required to make a minimum initial investment of $150,000; please read the Azure Managed Investment Account Agreement for complete details, including fees and expenses.

This commentary may contain forward-looking information, which reflects our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and do not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of March 31, 2026. There should be no expectation that such information will in all circumstances be updated, supplemented or revised, whether as a result of new information, changing circumstances, future events or otherwise.

This commentary is published by IG Wealth Management. It is provided as a general source of information. It is not intended to provide investment advice or as an endorsement of any investment. Some of the securities mentioned may be owned by IG Wealth Management or its mutual funds, or by portfolios managed by our external advisors. It may contain certain forward-looking statements regarding the market conditions which are based upon assumptions believed to be reasonable at the time of publishing. Every effort has been made to ensure that the material contained in the commentary is accurate at the time of publication, however, IG Wealth Management cannot guarantee the accuracy or the completeness of such material and accepts no responsibility for any loss arising from any use of or reliance on the information contained herein.

Past performance may not be repeated and is not indicative of future results. Actual performance may vary due to a range of factors including but not limited to current market conditions, timing of contributions and withdrawals, client-imposed restrictions, fees, expenses, tax considerations and other individual circumstances. There are no assurances that any mandate will achieve its objectives and/or avoid any losses.

Trademarks, including IG Wealth Management and IG Private Wealth Management, are owned by IGM Financial Inc. and licensed to subsidiary corporations.

©2026 IGWM Inc.