Mackenzie North American Value Equity

Mandate commentary

Q2 2026

Highlights

① The mandate returned 6.6%, underperforming its blended benchmark by 4.01 percentage points, despite strong security selection in industrials.

② Earnings strength helped markets absorb uncertainty.

③ Valuations and rates make selectivity more important.

Mandate overview

North American equities advanced strongly during the second quarter, with the blended benchmark (65% S&P/TSX Composite Index and 35% S&P 500 Index) returning approximately 10.6%. Information technology, financials and industrials led the advance, while energy and materials declined as oil and gold prices retreated from first-quarter highs. The second quarter featured a sharp rotation toward technology and financials, creating a relative headwind for value strategies with underweight technology and overweight commodity-sensitive holdings.

North American equities advanced strongly during the second quarter, with the blended benchmark (65% S&P/TSX Composite Index and 35% S&P 500 Index) returning approximately 10.6%. Information technology, financials and industrials led the advance, while energy and materials declined as oil and gold prices retreated from first-quarter highs. The second quarter featured a sharp rotation toward technology and financials, creating a relative headwind for value strategies with underweight technology and overweight commodity-sensitive holdings.

Relative performance was constrained primarily by sector allocation and stock selection in information technology, energy, financials and materials. Information technology was the largest relative detractor, reflecting the mandate’s underweight allocation and weaker security selection during the AI- and semiconductor-led rally. These effects were partially offset by strong stock selection in industrials and communication services.

Mandate: Mackenzie North American Value Equity portfolio stock review

Performance contributors

Royal Bank of Canada was the largest individual contributor, supported by strong second-quarter net income growth across its diversified businesses and a lower provision-for-credit-loss ratio.

Caterpillar contributed as resilient end-market demand, solid sales growth and robust order activity supported its shares. The holding contributed to industrials being the mandate’s largest source of relative value added during the quarter.

Performance detractors

Agnico Eagle Mines was the largest individual detractor. The holding declined as gold prices retreated from their March peak amid higher interest-rate expectations and a firmer U.S. dollar.

Canadian Natural Resources was another major detractor as oil prices declined from their first-quarter highs following progress toward reopening the Strait of Hormuz. The holding contributed to energy being a meaningful relative headwind.

Total gross returns:

Total return (CAD) | QTD | YTD | 1YR | 3YR | 5YR | SINCE INC. (NOV. 14, 2016) |

MACKENZIE NORTH AMERICAN VALUE EQUITY | 6.57

| 10.86

| 23.52

| 19.14

| 13.49

| 10.94

|

Mandate repositioning

During the quarter, the manager initiated positions in Palo Alto Networks, Visa, Coca-Cola, Carrier Global and Brookfield Infrastructure Partners, among others. It eliminated positions in CME Group, McKesson, McDonald’s, Union Pacific and Philip Morris, among others.

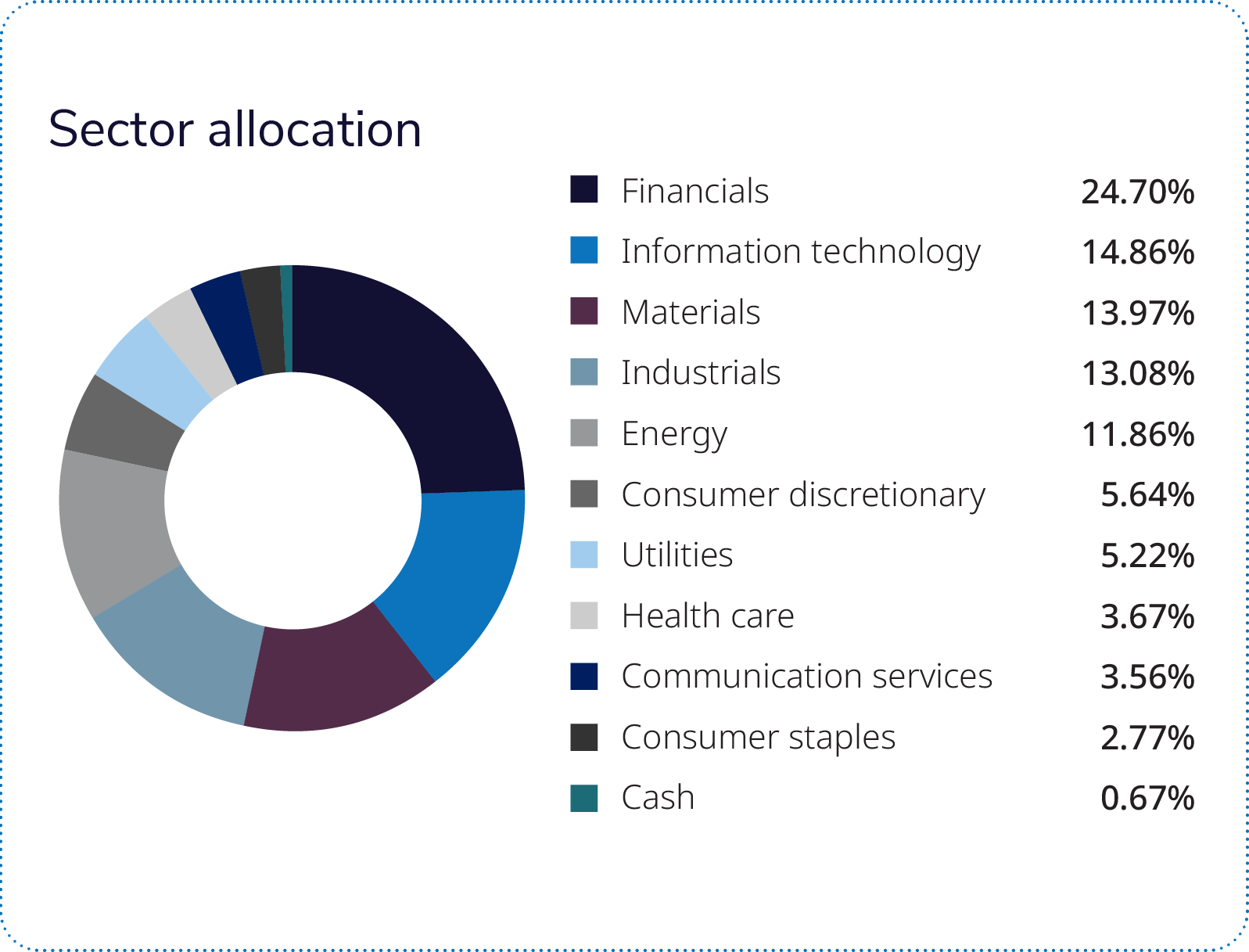

At quarter-end, the mandate’s largest sector overweights were industrials, materials and utilities, while it remained underweight information technology, financials and real estate. Energy exposure was close to the benchmark. The portfolio maintained its high-conviction, value-oriented approach, emphasizing companies with strong fundamentals, attractive valuations and improving earnings potential.

The strategy remains aligned with its investment philosophy, seeking undervalued businesses with improving fundamentals while maintaining diversification across sectors and geographies. The portfolio continues to balance cyclical opportunities with selective defensive exposures as market leadership evolves.

Market overview: earnings strength helped markets absorb uncertainty

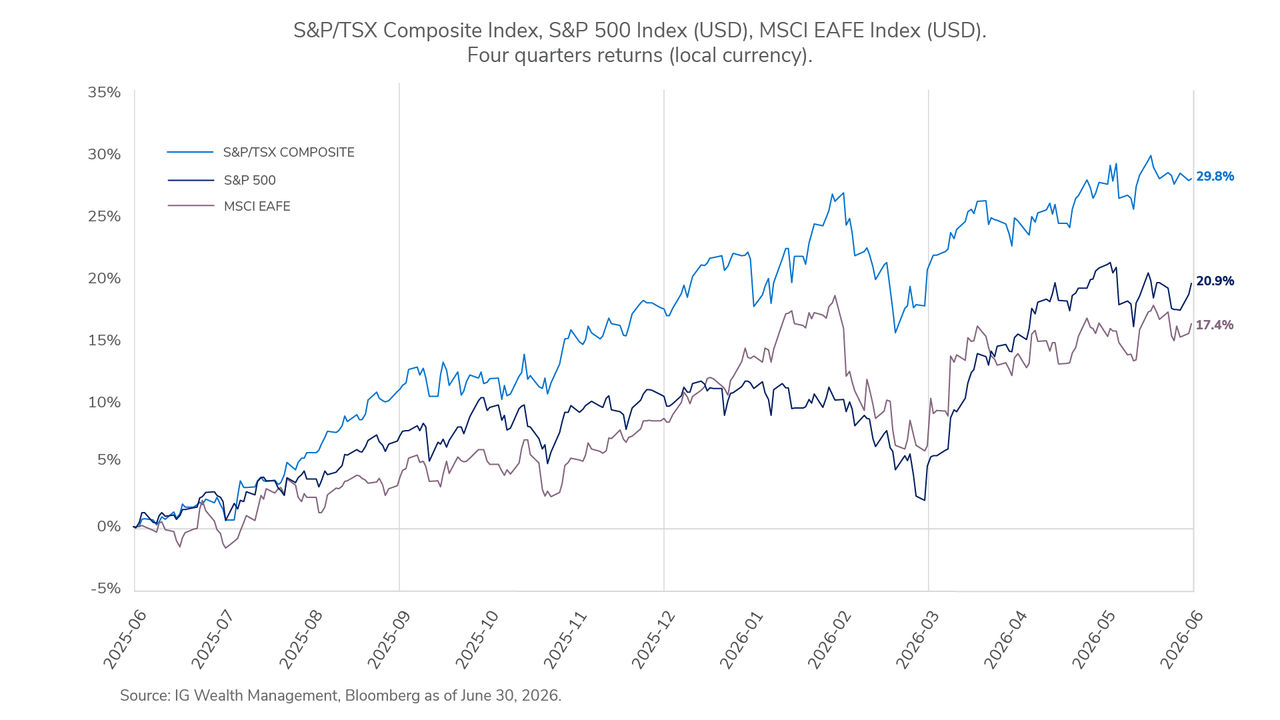

The second quarter of 2026 reinforced the resilience of financial markets. Investors faced conflict in the Middle East, commodity-price volatility, shifting interest-rate expectations and renewed inflation concerns, yet global equities continued to advance as corporate earnings and economic activity remained stronger than expected. The S&P 500 gained 14.9% in U.S.-dollar terms for the quarter, while the S&P/TSX Composite Index advanced 6.4%, supported by healthier earnings expectations and improving market breadth.

Canadian equities were led by a strong rebound in financials, as better-than-expected bank earnings, resilient credit quality and improved capital markets activity lifted sentiment. U.S. equities were supported by earnings strength rather than a simple risk-on rally, with Information Technology leading as AI infrastructure spending continued to anchor sentiment. International equities also contributed meaningfully, with emerging markets Korea and Taiwan benefitting from demand across the global technology supply chain.

Market outlook: valuations and rates make selectivity more important

Markets enter the second half of 2026 with fundamentals remaining broadly supportive, although elevated equity valuations leave less room for error. Earnings growth is likely to remain the key driver of returns, while inflation trends, central bank policy and interest-rate expectations will continue to shape market sentiment.

Across asset classes, diversification remains important. Canadian, international and emerging market equities offer exposure to distinct sources of growth, while higher yields in fixed income continue to provide a cushion against volatility. Selectivity remains key as investors balance opportunities against valuation and policy risks.

To discuss your investment strategy, speak to your IG Advisor.

Azure Managed Investments™ provides discretionary investment management services distributed by IG Wealth Management Inc., Investment dealer. We will manage your Azure Managed Investments Accounts on a segregated basis in accordance with your investment policy statement and the resulting mandate selected by you. Mandates will be managed by I.G. Investment Management, Ltd. and partner organizations. You are required to make a minimum initial investment of $150,000; please read the Azure Managed Investment Account Agreement for complete details, including fees and expenses.

This commentary may contain forward-looking information, which reflects our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and do not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of June 30, 2026. There should be no expectation that such information will in all circumstances be updated, supplemented or revised, whether as a result of new information, changing circumstances, future events or otherwise.

This commentary is published by IG Wealth Management. It is provided as a general source of information. It is not intended to provide investment advice or as an endorsement of any investment. Some of the securities mentioned may be owned by IG Wealth Management or its mutual funds, or by portfolios managed by our external advisors. It may contain certain forward-looking statements regarding the market conditions which are based upon assumptions believed to be reasonable at the time of publishing. Every effort has been made to ensure that the material contained in the commentary is accurate at the time of publication, however, IG Wealth Management cannot guarantee the accuracy or the completeness of such material and accepts no responsibility for any loss arising from any use of or reliance on the information contained herein.

Past performance may not be repeated and is not indicative of future results. Actual performance may vary due to a range of factors including but not limited to current market conditions, timing of contributions and withdrawals, client-imposed restrictions, fees, expenses, tax considerations and other individual circumstances. There are no assurances that any mandate will achieve its objectives and/or avoid any losses.

Trademarks, including IG Wealth Management and IG Private Wealth Management, are owned by IGM Financial Inc. and licensed to subsidiary corporations.

©2026 IGWM Inc.