Portfolio returns: Q2 2026

| Total Return | 1M | 3M | YTD | 1YR | 3YR | 5YR | 10YR | Since Inc. July 16, 2014 |

IG Core Portfolio – Global Income F | 0.54

| 1.10

| 0.90

| 2.63

| 3.74

| 1.27

| 2.08

| 2.72

|

Quartile rankings | 2 | 3 | 3 | 3 | 3 | 2 | 1 |

| Total Return | 1M | 3M | YTD | 1YR | 3YR | 5YR | 10YR | Since Inc. July 16, 2014 |

IG Core Portfolio – Global Income F | 0.54

| 1.10

| 0.90

| 2.63

| 3.74

| 1.27

| 2.08

| 2.72

|

Quartile rankings | 2 | 3 | 3 | 3 | 3 | 2 | 1 |

The second quarter delivered a changing of the guard at the Federal Reserve, an interim peace deal with Iran, and a bond market that finally stopped pricing hope. Canada spent the quarter debating whether it was in recession, with the Bank of Canada holding at 2.25% in April and June and core inflation near 2% with little energy pass-through. The broader economic data indicated that Canada's recent growth bounce was a temporary correction rather than a full recovery. Domestically, the labour market remains soft, business investment continued to contract due to tariff and Canada United States Mexico Agreement (CUSMA) uncertainties, and the mortgage reset cycle persists as a major drag.

The second quarter delivered a changing of the guard at the Federal Reserve, an interim peace deal with Iran, and a bond market that finally stopped pricing hope. Canada spent the quarter debating whether it was in recession, with the Bank of Canada holding at 2.25% in April and June and core inflation near 2% with little energy pass-through. The broader economic data indicated that Canada's recent growth bounce was a temporary correction rather than a full recovery. Domestically, the labour market remains soft, business investment continued to contract due to tariff and Canada United States Mexico Agreement (CUSMA) uncertainties, and the mortgage reset cycle persists as a major drag.

Government bond yields exhibited notable intra-quarter volatility during Q2 2026, peaking in mid-May before closing lower by the end of June. These fluctuations were catalyzed by specific macroeconomic events. The mid-May surge in yields was fueled by elevated energy prices and conversely an interim peace agreement with Iran alleviated energy-related inflation concerns. Yields were further depressed, led by softer-than-expected U.S. labour market data, which prompted markets to price in impending global monetary easing and exerted downward pressure on longer-term duration.

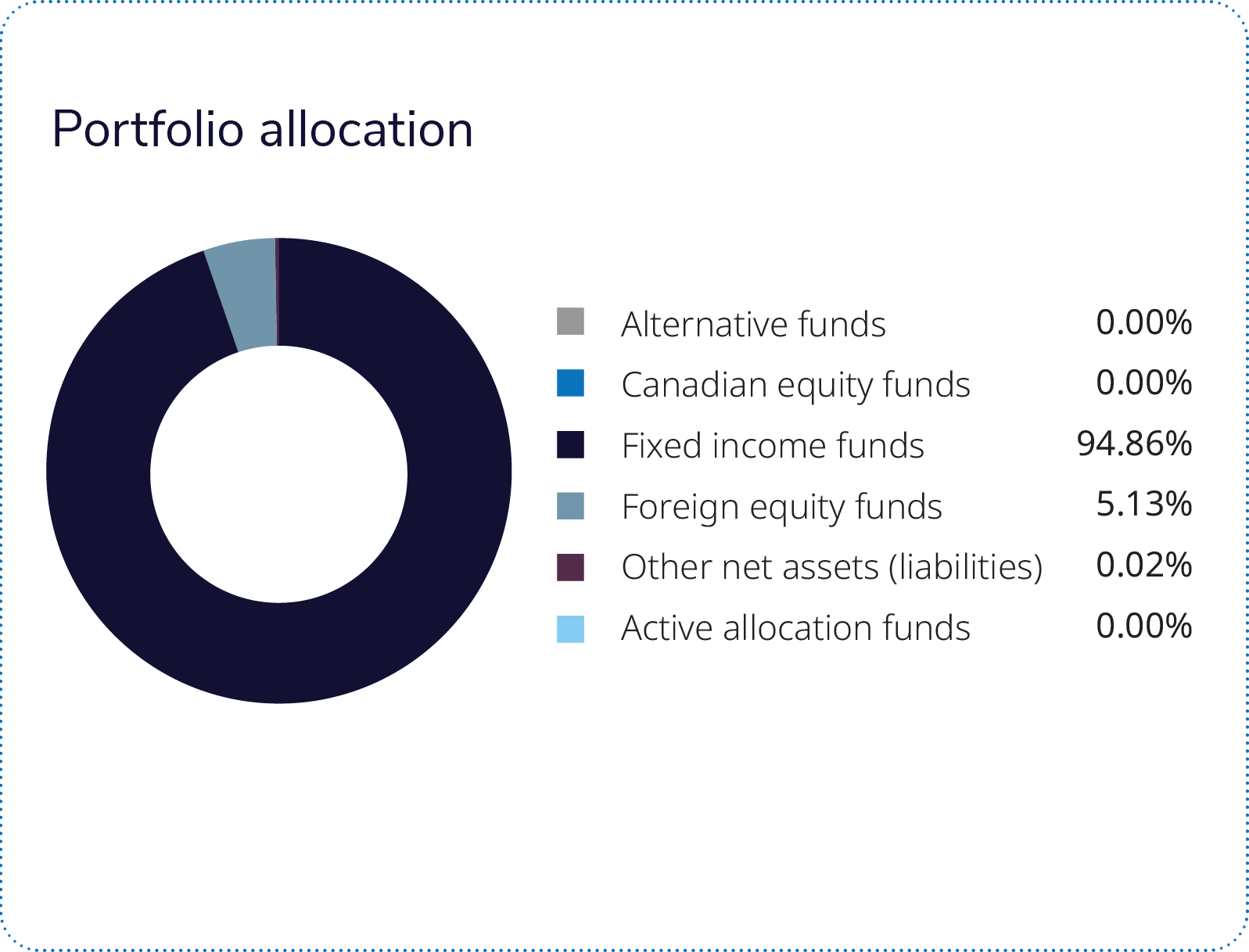

The portfolio modestly extended duration, driven primarily by a greater allocation to longer-maturity securities, resulting in greater exposure to long-end rates. Corporate duration declined over the quarter, suggesting the duration extension was achieved more through government-related exposures than through additional long-credit risk. Overall, the June positioning reflects a portfolio that was moderately more constructive on both duration and credit risk.

The fixed income segment delivered a solid overall portfolio contribution to returns for the quarter. Performance was overwhelmingly driven by the Mackenzie - IG Global Bond Pool. The Canadian credit and strategic bond allocations also contributed. The Mackenzie - IG Canadian Corporate Bond Pool was the second-largest driver, closely followed by the Mackenzie Canadian Strategic Fixed Income ETF.

Other core holdings, such as the Mackenzie AAA CLO ETF, Mackenzie Core Plus Global Fixed Income ETF and the Mackenzie North American Corporate Bond Fund delivered stable and synchronized support to overall performance.

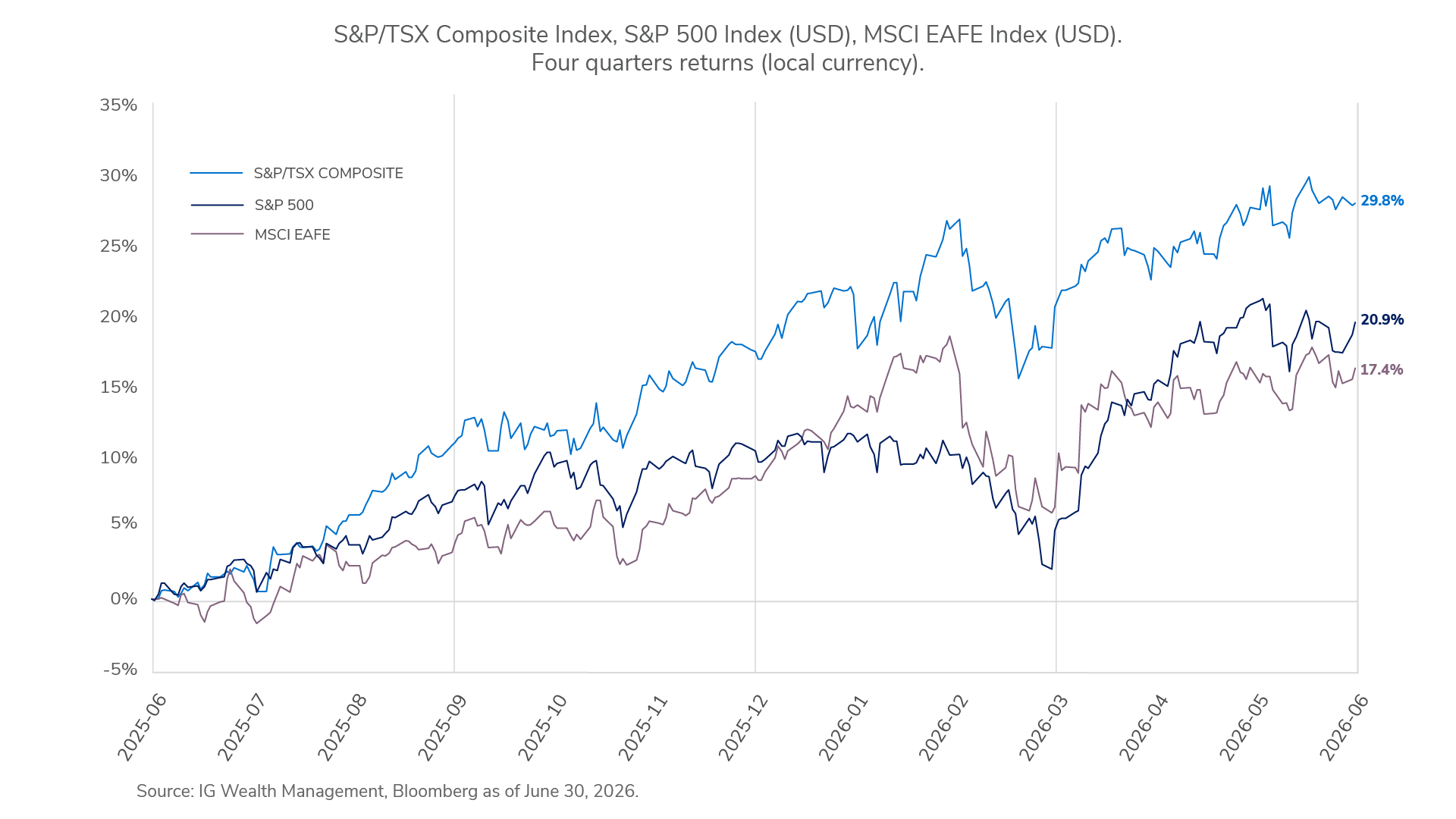

The second quarter of 2026 reinforced the resilience of financial markets. Investors faced conflict in the Middle East, commodity-price volatility, shifting interest-rate expectations and renewed inflation concerns, yet global equities continued to advance as corporate earnings and economic activity remained stronger than expected. The S&P 500 gained 14.9% in U.S.-dollar terms for the quarter, while the S&P/TSX Composite Index advanced 6.4%, supported by healthier earnings expectations and improving market breadth.

Canadian equities were led by a strong rebound in financials, as better-than-expected bank earnings, resilient credit quality and improved capital markets activity lifted sentiment. U.S. equities were supported by earnings strength rather than a simple risk-on rally, with Information Technology leading as AI infrastructure spending continued to anchor sentiment. International equities also contributed meaningfully, with emerging markets Korea and Taiwan benefitting from demand across the global technology supply chain.

Canadian fixed income presented an increasingly attractive opportunity as domestic economic headwinds diverged significantly from the stronger U.S. macro backdrop, and we expect the Bank of Canada to implement a 25 basis-point rate cut this year. The team remains positioned with an overall neutral duration stance, reflecting a balanced view on developed market rates. While the team maintains an allocation to 30-year U.S. real yields, this position is viewed primarily as a structural and cyclical carry opportunity rather than a directional duration call. Within emerging markets, the team continues to maintain a constructive bias, supported by the resilience of emerging market assets, despite periods of U.S. dollar strength. The portfolio retains long positions in Brazil and Mexico, where attractive risk-adjusted carry opportunities remain available. Brazil continues to be favoured for its high-yielding profile, while Mexico has demonstrated lower beta and greater resilience than many investors anticipated, reinforcing confidence in the position.

Commissions, fees and expenses may be associated with mutual fund investments. Read the prospectus and speak to an IG Advisor before investing. The rate of return is the historical annual compounded total return as of June 30, 2026, including changes in value and reinvestment of all dividends or distributions. It does not take into account sales, redemption, distribution, optional charges or income taxes payable by any securityholder that would have reduced returns. Mutual funds are not guaranteed, values change frequently and past performance may not be repeated. Mutual funds and investment products and services are offered through the Mutual Fund Division of IG Wealth Management Inc. (in Quebec, a firm in financial planning). And additional investment products and brokerage services are offered through the Investment Dealer, IG Wealth Management Inc. (in Quebec, a firm in financial planning), a member of the Canadian Investor Protection Fund.

This commentary may contain forward-looking information which reflects our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and do not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of June 30, 2026. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.

This commentary is published by IG Wealth Management. It represents the views of our Portfolio Managers and is provided as a general source of information. It is not intended to provide investment advice or as an endorsement of any investment. Some of the securities mentioned may be owned by IG Wealth Management or its mutual funds, or by portfolios managed by our external advisors. Every effort has been made to ensure that the material contained in the commentary is accurate at the time of publication, however, IG Wealth Management cannot guarantee the accuracy or the completeness of such material and accepts no responsibility for any loss arising from any use of or reliance on the information contained herein.

Trademarks, including IG Wealth Management and IG Private Wealth Management, are owned by IGM Financial Inc. and licensed to subsidiary corporations.

©2026 IGWM Inc.