Portfolio returns: Q1 2026

| Total Return | 1M | 3M | YTD | 1YR | 3YR | 5YR | 10YR | Since Inc. July 12, 2013 |

IG Core Portfolio – Income F | -0.44

| 0.49

| 0.49

| 2.78

| 4.30

| 2.51

| 2.67

| 2.76

|

Quartile rankings | 2 | 1 | 1 | 2 | 3 | 2 | 1 |

| Total Return | 1M | 3M | YTD | 1YR | 3YR | 5YR | 10YR | Since Inc. July 12, 2013 |

IG Core Portfolio – Income F | -0.44

| 0.49

| 0.49

| 2.78

| 4.30

| 2.51

| 2.67

| 2.76

|

Quartile rankings | 2 | 1 | 1 | 2 | 3 | 2 | 1 |

The first quarter of 2026 was defined by a volatile mix of persistent geopolitical friction in the Middle East and a robust, technology-driven growth narrative in the United States. While the period began with optimism following the resolution of the U.S. federal shutdown, market sentiment was quickly recalibrated as tensions between the U.S. and Iran escalated. This introduction of headline risk required a nimbler approach to duration and credit, as investors weighed the inflationary pressures of energy price volatility against the deflationary potential of a global growth shock.

The first quarter of 2026 was defined by a volatile mix of persistent geopolitical friction in the Middle East and a robust, technology-driven growth narrative in the United States. While the period began with optimism following the resolution of the U.S. federal shutdown, market sentiment was quickly recalibrated as tensions between the U.S. and Iran escalated. This introduction of headline risk required a nimbler approach to duration and credit, as investors weighed the inflationary pressures of energy price volatility against the deflationary potential of a global growth shock.

In the United States, the Federal Reserve maintained the federal funds rate at the 3.5%-3.75% target range. While the decision was widely anticipated, the narrative around projections revealed a central bank grappling with conflicting signals. On one hand, the "AI capital expenditure" theme has become a structural pillar of the domestic economy as the four largest tech titans are forecasted to spend more than $600 billion on capex this year.

On the other hand, the implications of the conflict in the Middle East remain a significant blind spot. Despite a brief suspension of hostilities in February, markets remained skeptical of a long-term diplomatic resolution. Consequently, inflation expectations were adjusted higher, with both personal consumption expenditures (PCE) and Core PCE now projected at 2.7% for the year. The Treasury yield curve experienced volatility during the quarter, as yields declined before rising later in the quarter.

The Canadian narrative diverged from that of the U.S., as domestic economic fragilities became more pronounced. The Bank of Canada (BoC) held its overnight rate steady at 2.25% in March, but the tone of policymakers shifted toward caution. Recent data confirmed that the Canadian economy contracted by 0.6% in the final quarter of 2025, and the labour market showed signs of cooling as the unemployment rate ticked up to 6.7% in February.

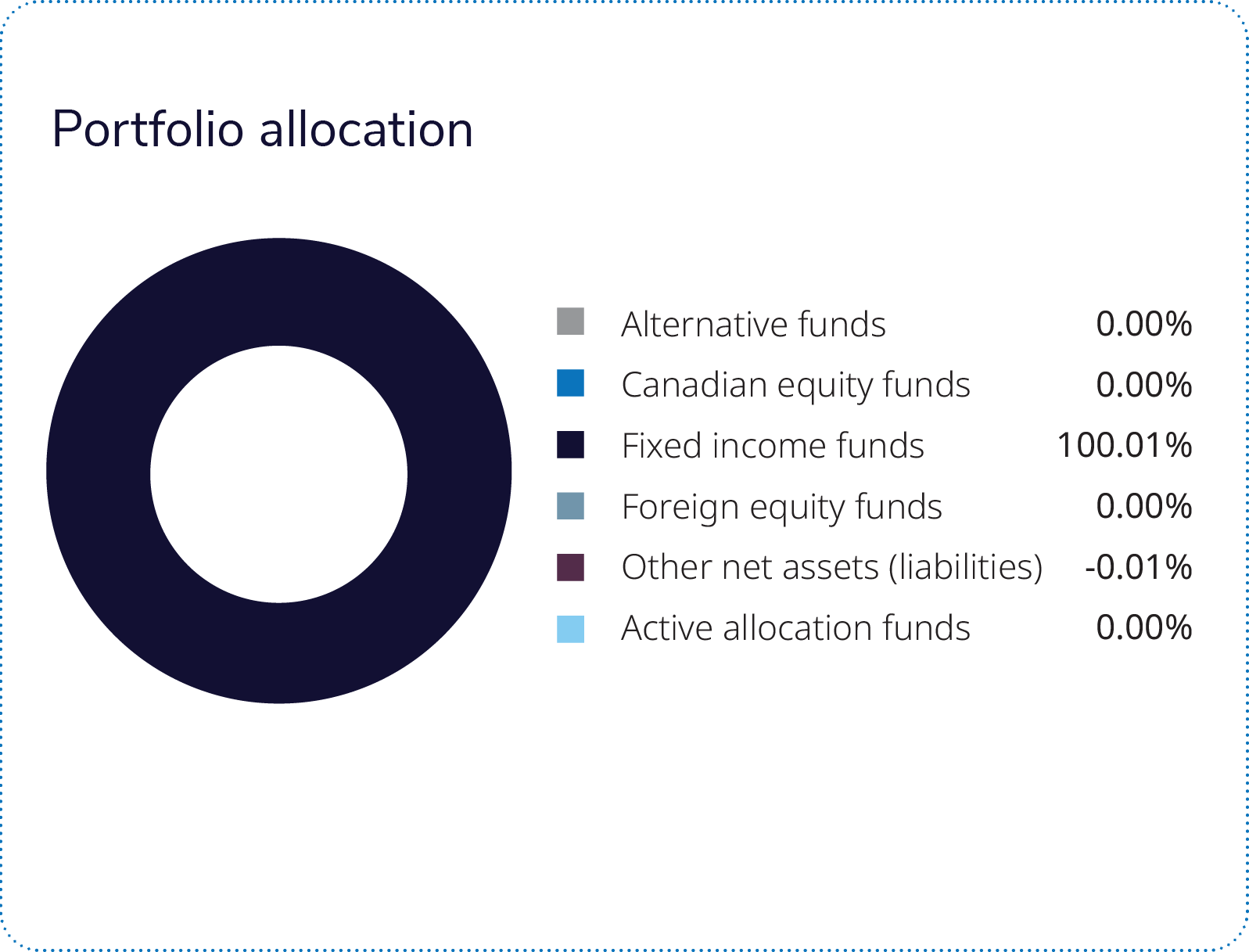

The IG Mackenzie Mortgage and Short Term Income Fund was the largest weighted allocation in the portfolio and largest contributor to performance. The IG Mackenzie Canadian Money Market Fund was the second largest weighted allocation in the portfolio and second largest contributor to performance.

During the period, the fund’s exposure to the Mackenzie - IG Canadian Corporate Bond Pool remained consistent at 15.3%. The fund’s allocation to the IG Mackenzie Canadian Money Market Fund ended the period at 18.4%. The fund ended the period with a 3.1% allocation to the Mackenzie High Quality Floating Rate Fund.

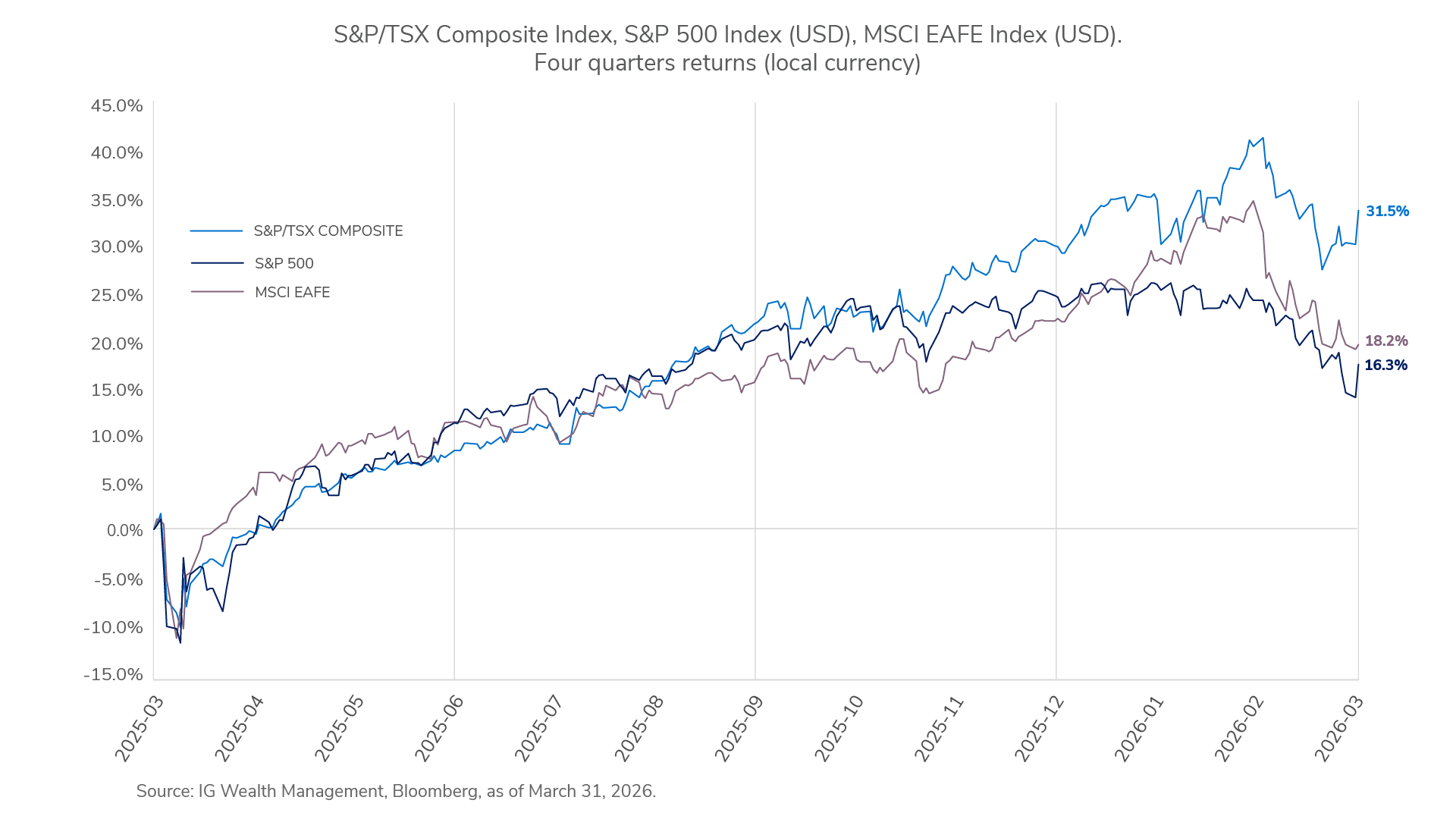

The first quarter of 2026 began with supportive economic momentum; improving manufacturing, a stabilizing U.S. housing backdrop and contained inflation. However, this quickly pivoted as the conflict in the Middle-East involving Iran — along with trade disruption around the Strait of Hormuz — pushed energy commodities higher. The energy shock drove volatility across global equities, yet the underlying backdrop proved more resilient than headlines implied, reinforcing the value of diversification.

Canadian equities were resilient, as higher crude oil prices supported the energy sector and helped offset weaknesses in rate-sensitive areas. Defensive sectors, dividends and real-asset exposure provided additional insulation versus many global peers. U.S. fundamentals remained solid, but sentiment weakened as oil lifted inflation expectations. Investors rotated away from expensive, rate-sensitive growth stocks, making performance more about a valuation reset than deteriorating earnings.

Looking ahead, we are maintaining a long front-end bias in Canada. Our thesis remains that Canada is entering a housing-led downturn, where a combination of falling rents and tighter financing will prompt the Bank of Canada to initiate rate cuts of 0.25-0.5 of a percentage point toward mid-year. In the U.S., our positioning was more tactical. We began the year underweight duration but moved to neutral as the Middle East conflict escalated. Within credit, we are maintaining an overweight stance in investment grade. In high yield, we continue to express a high-conviction in the aerospace and defence sectors. In an environment of remilitarization and increased fiscal defence outlays, companies in these sectors offer attractive risk-adjusted profiles. As we move into the second quarter, we remain disciplined, prioritizing quality as the market continues to navigate this period of heightened geopolitical and fiscal uncertainty.

Commissions, fees and expenses may be associated with mutual fund investments. Read the prospectus and speak to an IG Advisor before investing. The rate of return is the historical annual compounded total return as of March 31, 2026, including changes in value and reinvestment of all dividends or distributions. It does not take into account sales, redemption, distribution, optional charges or income taxes payable by any securityholder that would have reduced returns. Mutual funds are not guaranteed, values change frequently and past performance may not be repeated. Mutual funds and investment products and services are offered through the Mutual Fund Division of IG Wealth Management Inc. (in Quebec, a firm in financial planning). And additional investment products and brokerage services are offered through the Investment Dealer, IG Wealth Management Inc. (in Quebec, a firm in financial planning), a member of the Canadian Investor Protection Fund.

This commentary may contain forward-looking information which reflects our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and do not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of March 31, 2026. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.

This commentary is published by IG Wealth Management. It represents the views of our Portfolio Managers and is provided as a general source of information. It is not intended to provide investment advice or as an endorsement of any investment. Some of the securities mentioned may be owned by IG Wealth Management or its mutual funds, or by portfolios managed by our external advisors. Every effort has been made to ensure that the material contained in the commentary is accurate at the time of publication, however, IG Wealth Management cannot guarantee the accuracy or the completeness of such material and accepts no responsibility for any loss arising from any use of or reliance on the information contained herein.

Trademarks, including IG Wealth Management and IG Private Wealth Management, are owned by IGM Financial Inc. and licensed to subsidiary corporations.

©2026 IGWM Inc.