Portfolio returns: Q2 2026

| Total Return | 1M | 3M | YTD | 1YR | 3YR | 5YR | 10YR | Since Inc. (Jun 22, 2020) |

iProfile Portfolio – Global Equity I | 2.48

| 12.48

| 12.69

| 24.74

| 19.89

| 12.83

| 14.75

| |

Quartile rankings | 2 | 3 | 2 | 2 | 2 | 1 |

| Total Return | 1M | 3M | YTD | 1YR | 3YR | 5YR | 10YR | Since Inc. (Jun 22, 2020) |

iProfile Portfolio – Global Equity I | 2.48

| 12.48

| 12.69

| 24.74

| 19.89

| 12.83

| 14.75

| |

Quartile rankings | 2 | 3 | 2 | 2 | 2 | 1 |

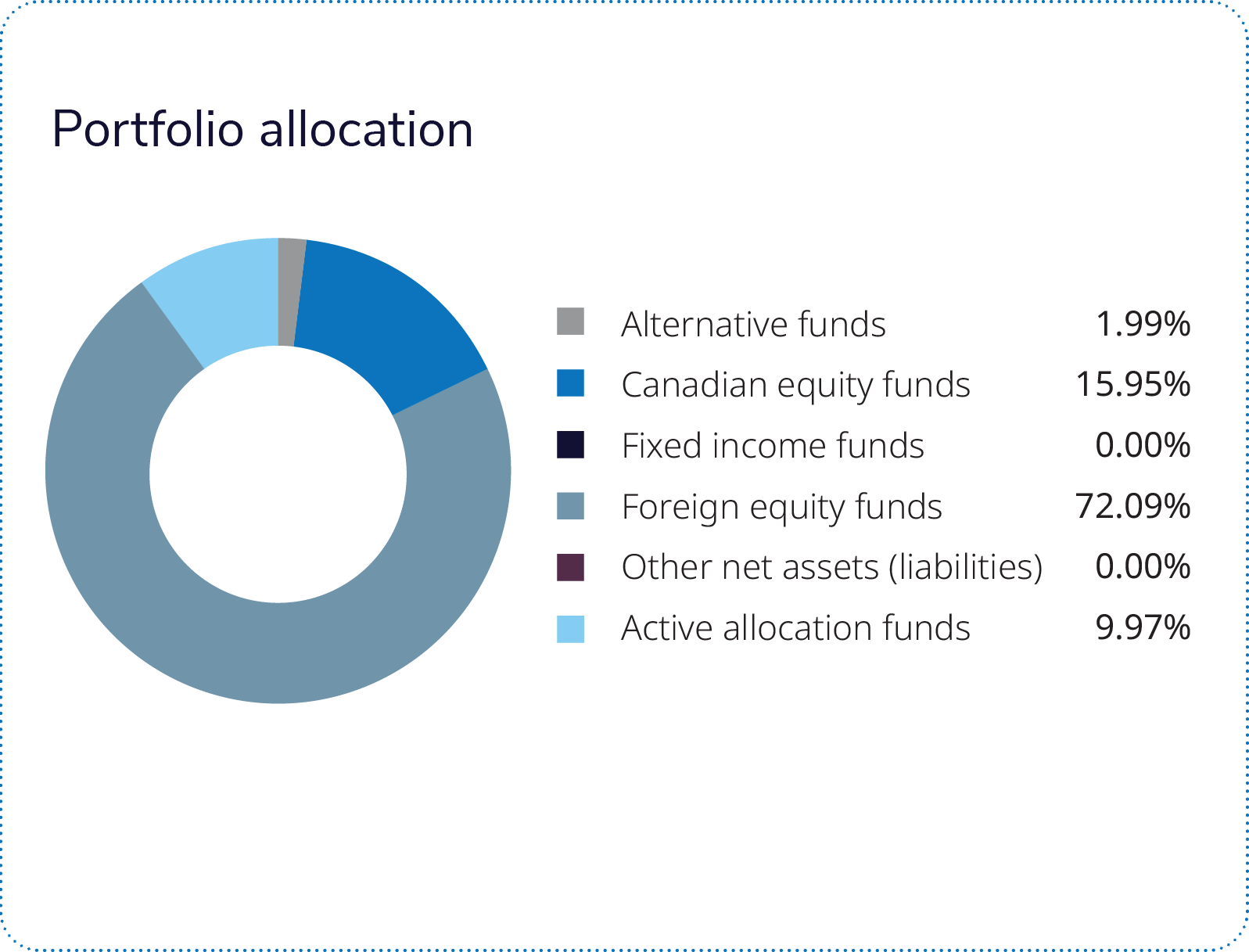

The iProfileTM Portfolio – Global Equity, Series I, rose over by 12.5% in the second quarter of 2026, underperforming its global equity peer group median (14.0%). Global equity markets were led by a narrow rally in semiconductor and technology hardware names as investor enthusiasm for artificial intelligence (AI) continued to accelerate. While the portfolio benefited from broad-based gains across all component pools, it did not fully participate in the strongest-performing areas of the market.

The iProfileTM Portfolio – Global Equity, Series I, rose over by 12.5% in the second quarter of 2026, underperforming its global equity peer group median (14.0%). Global equity markets were led by a narrow rally in semiconductor and technology hardware names as investor enthusiasm for artificial intelligence (AI) continued to accelerate. While the portfolio benefited from broad-based gains across all component pools, it did not fully participate in the strongest-performing areas of the market.

The iProfile U.S. Equity Private Pool was the largest contributor to portfolio performance, returning 15.6% and adding approximately 4.0% to overall results. Strong gains from technology-related holdings and broader equity market strength supported returns, with Advanced Energy Industries among the notable contributors. These gains were partially offset by weakness in holdings such as Charter Communications.

The iProfile ETF Private Pool and iProfile International Equity Private Pool were also significant contributors, each adding approximately 2.1% to portfolio returns. Within international equities, semiconductor-related holdings such as Taiwan Semiconductor Manufacturing, Tokyo Electron and ASML Holding benefited from continued global demand for advanced chip technology. However, the pool's exposure to several of the quarter's strongest-performing technology companies was lower than that of its benchmark, which weighed on relative performance.

The iProfile Emerging Markets Private Pool was the strongest-performing equity allocation in the portfolio, rising approximately 29.4% during the quarter. Returns were driven by significant gains in technology and semiconductor companies, particularly SK Hynix, which benefited from continued AI-related investment and demand for advanced memory chips. Delivery Hero was another strong contributor to performance. These gains were partially offset by weakness in holdings such as Petroleo Brasileiro and Genpact.

The iProfile Active Allocation Private Pool and iProfile Canadian Equity Private Pool also contributed positively to results. Canadian equities benefited from strong performance in industrial companies such as Bombardier and TFI International. Energy holdings, including Suncor Energy and Canadian Natural Resources, detracted from returns as oil prices declined during the quarter.

Among the portfolio's smaller allocations, the Mackenzie – IG Low Volatility U.S. Equity Pool made a modest positive contribution, while the Mackenzie Global Macro Fund, Wellington – IG Global Equity Hedge Pool and Mackenzie – IG Low Volatility Emerging Markets Equity Pool also added to returns. The BlackRock – IG Low Volatility International Equity Pool was the only component to generate a slightly negative return, although its impact on overall portfolio results was limited given its relatively small weighting within the portfolio.

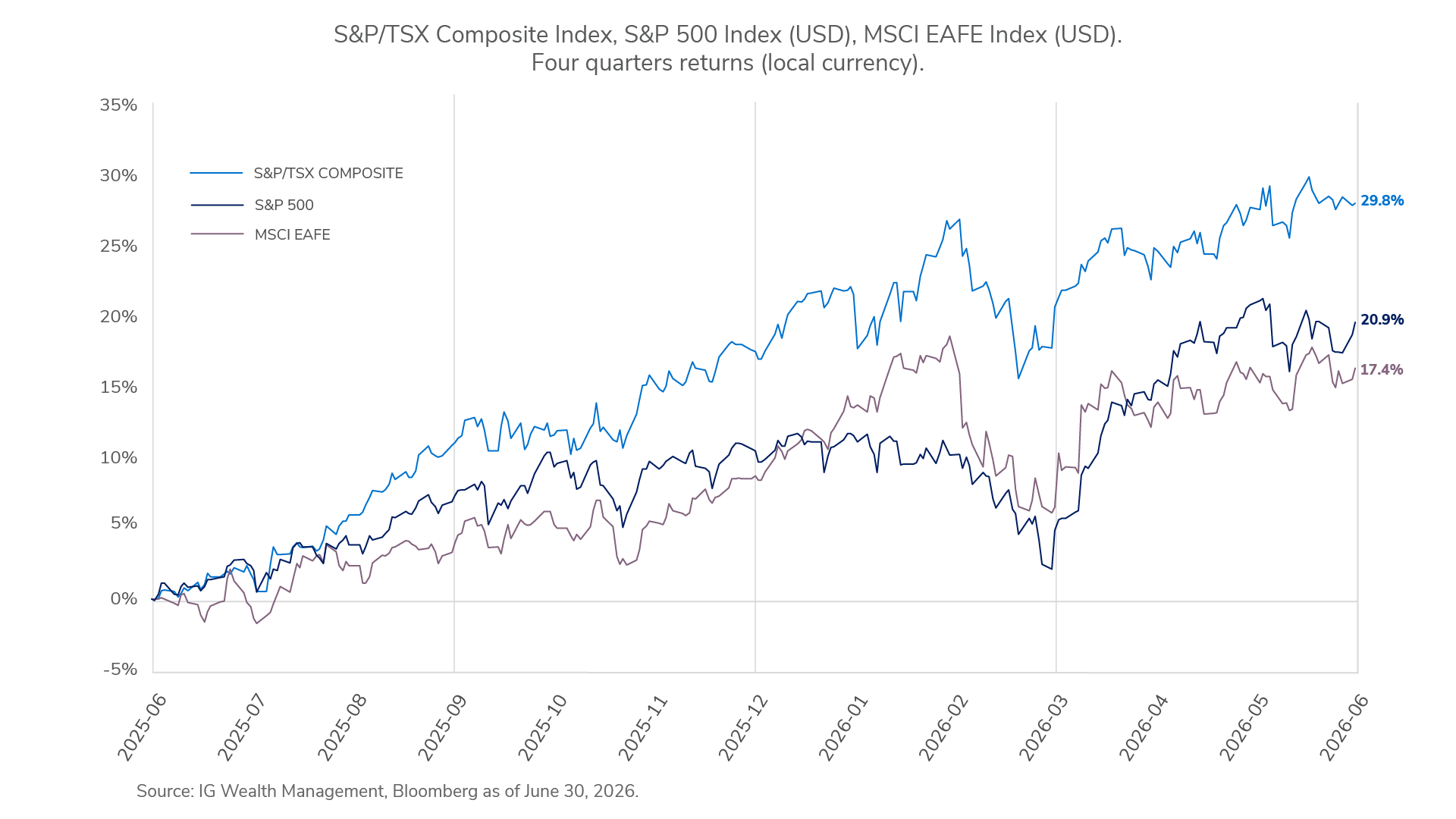

The second quarter of 2026 reinforced the resilience of financial markets. Investors faced conflict in the Middle East, commodity-price volatility, shifting interest-rate expectations and renewed inflation concerns, yet global equities continued to advance as corporate earnings and economic activity remained stronger than expected. The S&P 500 gained 14.9% in U.S.-dollar terms for the quarter, while the S&P/TSX Composite Index advanced 6.4%, supported by healthier earnings expectations and improving market breadth.

Canadian equities were led by a strong rebound in financials, as better-than-expected bank earnings, resilient credit quality and improved capital markets activity lifted sentiment. U.S. equities were supported by earnings strength rather than a simple risk-on rally, with Information Technology leading as AI infrastructure spending continued to anchor sentiment. International equities also contributed meaningfully, with emerging markets Korea and Taiwan benefitting from demand across the global technology supply chain.

Markets enter the second half of 2026 with fundamentals remaining broadly supportive, although elevated equity valuations leave less room for error. Earnings growth is likely to remain the key driver of returns, while inflation trends, central bank policy and interest-rate expectations will continue to shape market sentiment.

Across asset classes, diversification remains important. Canadian, international and emerging market equities offer exposure to distinct sources of growth, while higher yields in fixed income continue to provide a cushion against volatility. Selectivity remains key as investors balance opportunities against valuation and policy risks.

Commissions, fees and expenses may be associated with mutual fund investments. Read the prospectus and speak to an IG Advisor before investing. The rate of return is the historical annual compounded total return as of June 30, 2026, including changes in value and reinvestment of all dividends or distributions. It does not take into account sales, redemption, distribution, optional charges or income taxes payable by any securityholder that would have reduced returns. Mutual funds are not guaranteed, values change frequently and past performance may not be repeated. Mutual funds and investment products and services are offered through the Mutual Fund Division of IG Wealth Management Inc. (in Quebec, a firm in financial planning). And additional investment products and brokerage services are offered through the Investment Dealer, IG Wealth Management Inc. (in Quebec, a firm in financial planning), a member of the Canadian Investor Protection Fund.

This commentary may contain forward-looking information which reflects our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and do not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of June 30, 2026. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.

This commentary is published by IG Wealth Management. It represents the views of our Portfolio Managers and is provided as a general source of information. It is not intended to provide investment advice or as an endorsement of any investment. Some of the securities mentioned may be owned by IG Wealth Management or its mutual funds, or by portfolios managed by our external advisors. Every effort has been made to ensure that the material contained in the commentary is accurate at the time of publication, however, IG Wealth Management cannot guarantee the accuracy or the completeness of such material and accepts no responsibility for any loss arising from any use of or reliance on the information contained herein.

Trademarks, including IG Wealth Management and IG Private Wealth Management, are owned by IGM Financial Inc. and licensed to subsidiary corporations.

©2026 IGWM Inc.