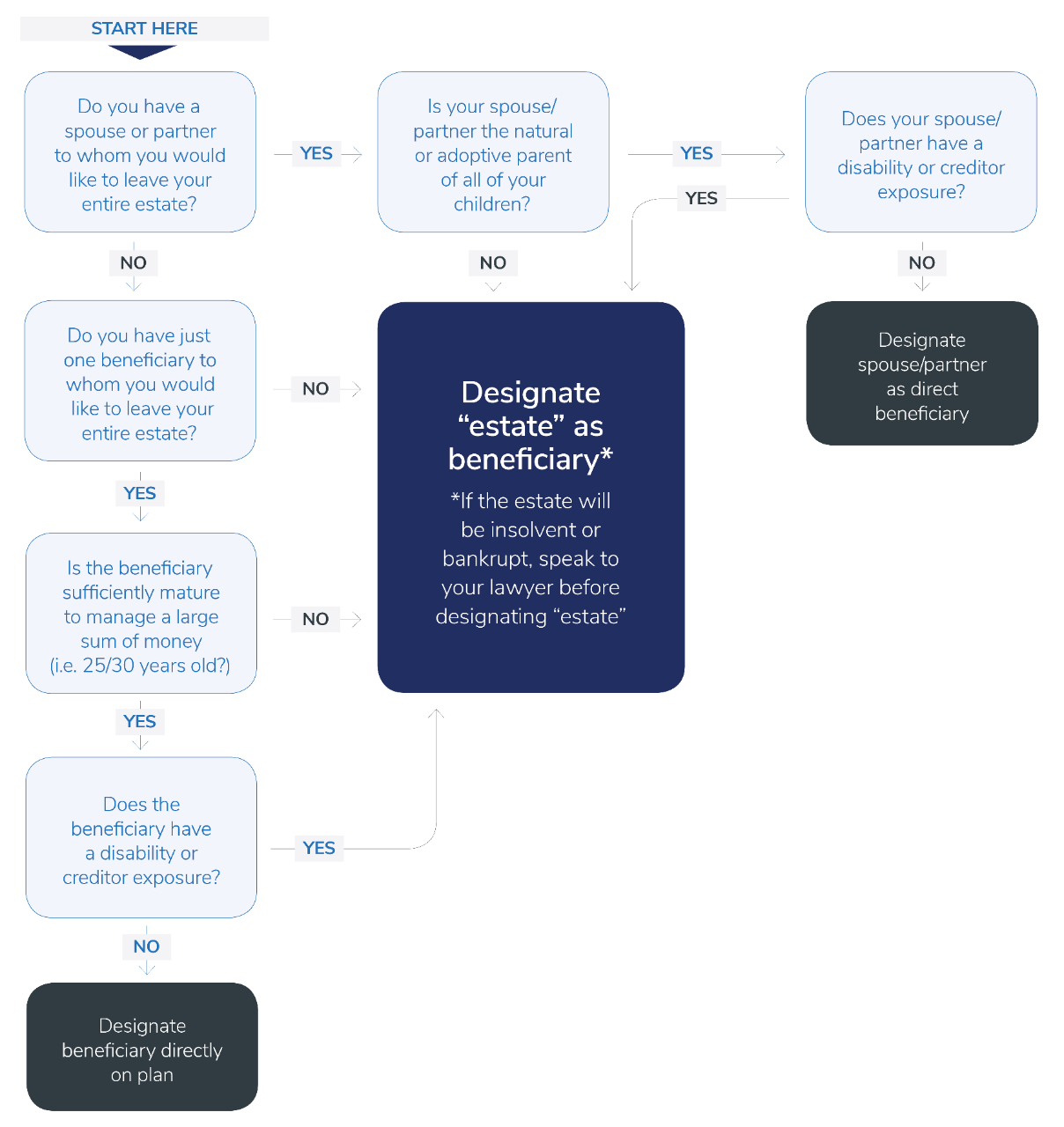

However, designating a direct beneficiary is not recommended for many plan/policy owners, where they have non-traditional or unique family situations, as it can lead to unfavourable tax implications for beneficiaries. We’ve created a beneficiary designations decision tree to help you understand the factors you should consider in designating a plan/policy beneficiary.

Generally, direct beneficiary designations are most appropriate in the following circumstances:

- When you’re in a first marriage or relationship and want to leave your entire estate to your surviving spouse/partner.

- When you will not be survived by a spouse/partner, and you want to leave your entire estate to only one beneficiary (e.g., an only child or just one charity); or

- Where there is a concern that your estate may be bankrupt or insolvent (and you want assets to pass outside of your estate to avoid exposure to estate creditors).

However, designating direct beneficiaries is usually not that straightforward. There are other important factors to consider, and designating a direct beneficiary is strongly discouraged in these situations:

- Where any of your beneficiaries is a minor (or young adult)

- Where any of your beneficiaries is person with a disability

- When you are part of a blended families (i.e., you are in a relationship where your spouse or partner is not the natural or adoptive parent of all of your children)

- Where there are multiple beneficiaries (e.g., you have more than one child)

- Where there are secondary, alternate or contingent designations; or

- In situations where a beneficiary has creditor exposure (e.g., a business owner)

While this article and decision tree address several common questions about designating plan/policy beneficiaries, every family has unique dynamics and tax planning needs. To properly structure an estate plan that best reflects your wishes, there are additional factors to consider. Always speak to an estates lawyer and a financial advisor before designating a beneficiary of any of your assets. For more information on this topic, please ask your IG Advisor for a copy of our white papers, “Beneficiary designations: The dos and don’ts” and “Estate Planning Guide.”

Written and published by IG Wealth Management as a general source of information only. Not intended as a solicitation to buy or sell specific investments, or to provide tax, legal or investment advice. Seek advice on your specific circumstances from an IG Advisor. Trademarks, including IG Wealth Management and IG Private Wealth Management, are owned by IGM Financial Inc. and licensed to its subsidiary corporations.