The UHT is an annual 1% tax on the value of underused or vacant residential property in Canada. The deadline for the first ever UHT returns (for persons who owned property on December 31, 2022) was extended to April 30, 2024, but subsequent returns will be due on April 30 of the following year. For example, 2024 returns were due April 30, 2025, 2025 returns will be due April 30, 2026, and so on.

The introduction of the Underused Housing Tax

The federal Underused Housing Tax Act came into force as of January 1, 2022, and applies a 1% tax on the value of underused or vacant residential real estate in Canada held by non-resident, non-Canadian owners. The property’s value is based on the greater of the assessed value or the most recent sale price on or before December 31 of that year.

Here is a general overview of who has to file a return and what exemptions may be available.

Who has to file a return?

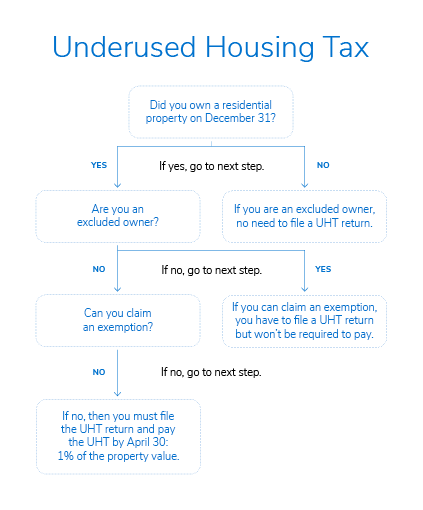

All registered owners, unless they are an excluded owner, are required to file a return (the new UHT-2900) along with a complete declaration of current use for each Canadian residential property they own.

An excluded owner includes:

- An individual Canadian citizen or permanent resident.

- A publicly traded Canadian corporation.

- A trustee of a widely-held trust, mutual fund trust or real estate investment trust.

- A registered charity, co-operative housing corporation, municipal organization, public institution or governing body.

- A Canadian corporation with less than 10% foreign ownership.

- A partnership where all members are either excluded owners or Canadian corporations with less than 10% foreign ownership.

- A trust where all beneficiaries are either excluded owners or Canadian corporations with less than 10% of foreign ownership.

- An individual Canadian citizen or permanent resident who died during the year or is personal representative of an owner who died.

Overall, corporations with more than 90% Canadian ownership, partnerships with all Canadian partners, and inter-vivos trusts with all Canadian beneficiaries will not be subject to UHT. All other taxpayers not meeting the definition of an excluded owner will be considered an “affected owner” and are required to file a UHT return.

If an affected owner does not file the UHT return by the deadline, late filing penalties are equal to the greater of:

- $1,000 for individuals or $2,000 for non-individuals; and

- The total of:

- 5% of any related UHT for the year, and

- 3% of any related UHT for the year multiplied by the number of months the return is late.

Who must pay the tax?

Affected owners who have to file a return can claim an exemption for a residential property (including a detached house, semi-detached house, rowhouse or condo unit) that is one of the following:

- A primary place of residence for the owner, owner’s spouse, common-law partner or child.

- A new owner of the property in the calendar year.

- If the property is not the primary place of residence, but is used as a residence because of the employment of the owner or a person related to the owner.

- A property occupied at least 180 days of the year by one of the following:

- An unrelated individual under a written agreement.

- A family member paying fair rent under a written agreement.

- The owner or their spouse who is in Canada via a work permit.

- The owner’s Canadian citizen/permanent resident spouse, common-law partner or child.

- Not accessible or suitable to be lived in year-round or seasonably inaccessible.

- Uninhabitable for a certain number of days due to a disaster, hazardous conditions or renovations.

- Newly constructed and not substantially completed before April of the calendar year.

- A vacation property in an eligible part of Canada, used for at least 28 days in a calendar year.

However, these owners would still need to file a return to claim an exemption and if these owners held more than one property subject to the UHT, a return would need to be filed for each property.

As an example, an American resident who owns Canadian vacation property would be required to file a UHT tax return and claim an exemption to avoid paying UHT, unless they were Canadian citizens, in which case they wouldn’t have to file a return. If the American resident owns multiple Canadian vacation properties, a UHT return would need to be filed for each corresponding property and claim any available exemptions.

If in doubt, ask for advice

If you owned a residential property (especially if you owned that property in a corporation, partnership or trust) on December 31, we encourage you to speak to your accountant to find out if you need to file a return and whether you can take advantage of one of the exemptions available.

Written and published by IG Wealth Management as a general source of information only. Not intended as a solicitation to buy or sell specific investments, or to provide tax, legal or investment advice. Seek advice on your specific circumstances from an IG Advisor. Trademarks, including IG Wealth Management and IG Private Wealth Management, are owned by IGM Financial Inc. and licensed to subsidiary corporations.